Regulation, use cases, and $30B in tokenized real world assets (RWAs).

Published: October 8, 2025

In Q3 2025, the tokenized real-world asset (RWA) market crossed $30B, led by demand for yield-bearing assets. Regulatory foundations advanced in major jurisdictions including the US, Singapore, Hong Kong, and the UAE, while institutions such as BlackRock, Franklin Templeton, and Fidelity continued to drive issuance volumes. At the same time, firms like DBS Bank and Binance expanded use cases for tokenized RWAs.

In this Q3 2025 RWA tokenization market recap, we review RWA tokenization updates from Q3 2025, including key market developments, the regulatory shifts shaping adoption, and how infrastructure and stablecoins are supporting institutional use cases.

Key Takeaways:

- Tokenized assets crossed $30B, driven by private credit (~$17B) and U.S. Treasuries (~$7.3B), with commodities and institutional alternative funds (~$2B each) gaining traction.

- Regulatory progress advanced across major hubs: the U.S. (Project Crypto, GENIUS Act), UK (Digital Securities Sandbox), Singapore & Australia (Project Guardian, Project Acacia pilots), Japan (Crypto bill by 2026), and Hong Kong (Basel flexibility for banks using stablecoins).

- Institutional activity expanded: BlackRock evaluating ETF tokenization, Nasdaq filing to list tokenized stocks, DBS Bank integrating tokenized MMFs as collateral, Goldman Sachs and BNY Mellon issuing tokenized MMFs, Binance adopting tokenized Treasuries in off-exchange settlement, and MUFG preparing real estate tokenization.

- Stablecoins strengthened their role as settlement infrastructure, paired with Treasuries and MMFs in repo and collateral flows, as prudential frameworks emerged in the U.S., Japan, Hong Kong, and South Korea.

RWA Tokenization Market Size: $30B and Rising

Tokenized real-world assets (RWAs) crossed $30 billion in market size this quarter, driven by institutional demand for on-chain fixed income and private credit strategies. This figure reflects a roughly 10x increase from 2022 levels, when total tokenized RWA value stood at $2.9 billion.

The composition of that growth matters: capital is concentrating in income products that fit existing workflows and governance, rather than speculative categories.

.webp)

Private credit and U.S. treasuries continue to dominate the RWA market structure:

- Private credit (~$17B tokenized as of September 2025): Tokenization is increasingly applied to credit funds and short-duration financing structures, reflecting institutional appetite for yield-bearing assets with enhanced distribution and operational efficiency.

- U.S. Treasuries (~$7.3B tokenized as of September 2025): Treasuries remain a foundational asset class in tokenized finance due to their low-risk profile, deep liquidity, and relevance in high-rate environments. They also serve as base collateral for settlement and financing flows, reinforcing their role as on-chain “cash equivalents.”

Meanwhile, commodities and institutional alternative funds are seeing steady growth:

- Commodities (~$2B tokenized as of September 2025): Gold and carbon credits are increasingly tokenized, especially for use in payments, custody, and short-term liquidity solutions.

- Alternative Funds (~$2B tokenized as of September 2025): Institutional vehicles such as tokenized money market funds (MMFs) are being integrated into collateral and treasury management workflows. These vehicles align with how institutions already manage liquidity and cash segmentation.

Taken together, Q3’s asset mix indicates that tokenization is scaling first where product familiarity, standardized documentation, and operational efficiency converge.

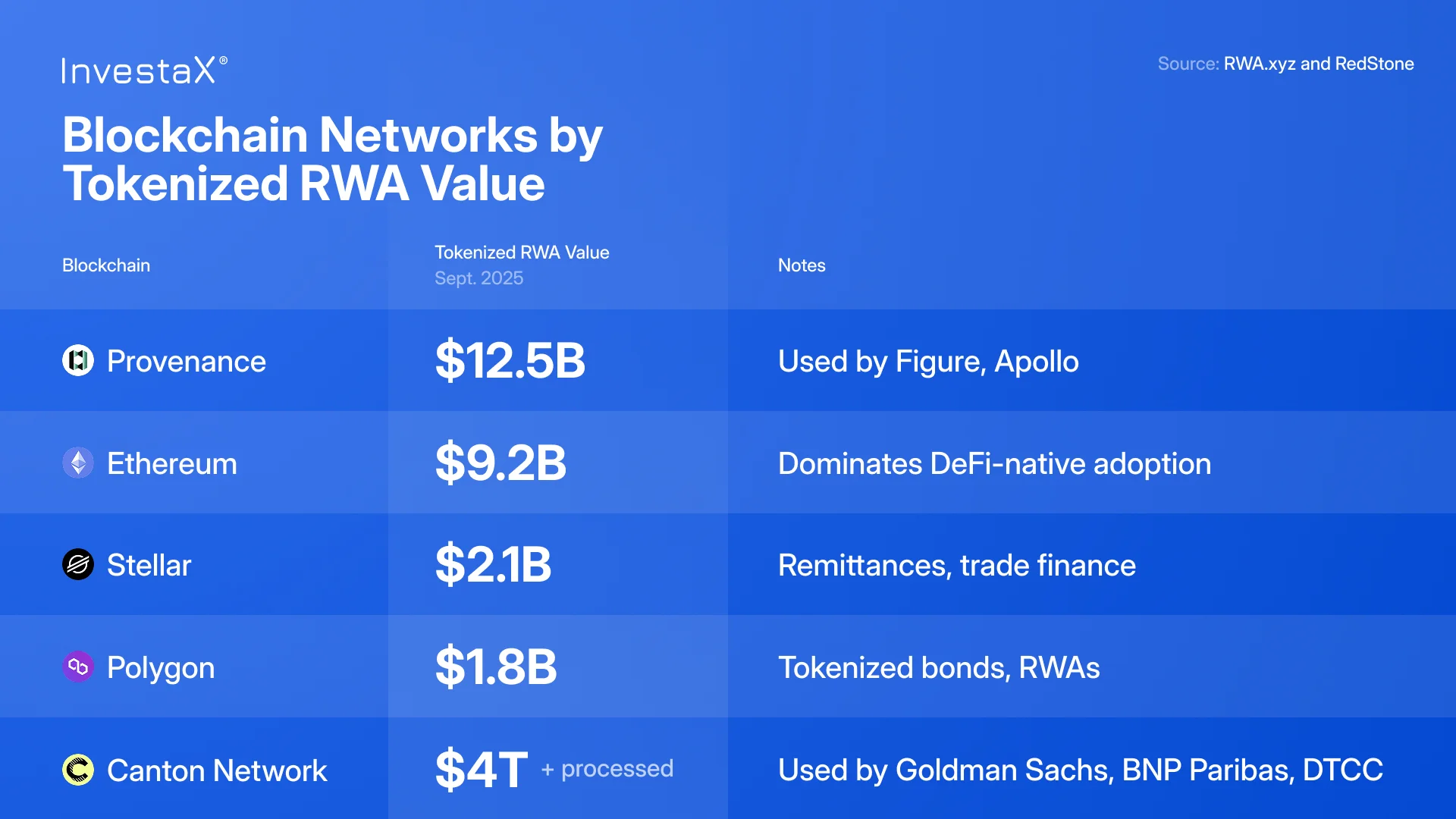

Infrastructure League Table

The RWA ecosystem is distributed across both public and permissioned blockchains.

Provenance and Ethereum account for a large share of visible tokenized asset volume. Provenance currently leads with over $12 billion in RWAs. Ethereum hosts key issuers such as BlackRock, Ondo, Backed, and Franklin Templeton. Issuer concentration on these rails reflects where distribution, custody, and wallet tooling are already enterprise-ready.

But permissioned infrastructure is also expanding. According to RedStone’s Real-World Assets in Onchain Finance Report, Canton Network, backed by Goldman Sachs, BNP Paribas, and DTCC, now processes over $4 trillion in tokenized transactions, including $2 trillion monthly in Treasury repo flows.

This split architecture is practical: public chains carry distribution and composability, while permissioned networks align to bilateral settlement, privacy, and counterparty controls.

Market Movements Across The Globe

With the core rails hardening, Q3 also brought measurable traction across regulatory and market fronts. The result is a shift from pilots to early operational adoption, especially in fixed income and credit.

Below are the curated RWA tokenization updates from Q3 2025.

1. Regulatory Shifts Set the Foundation for Scale

The third quarter brought stronger alignment between policymakers and tokenization efforts, especially in major financial centers. Some jurisdictions like the U.S. are working to integrate tokenized instruments into existing securities laws, while others like Singapore and Australia are prioritizing supervised pilots. Most initiatives emphasized “same activity, same risk, same regulatory outcome,” which is consistent with how institutions prefer to scale new rails.

United States

- U.S. lawmakers advanced landmark legislation under "Crypto Week," including the GENIUS Act, the CLARITY Act, and the Anti-CBDC Surveillance State Act.

- The U.S. SEC’s crypto task force held discussions with SIFMA regarding regulatory treatment of tokenized securities and digital asset products.

- The SEC also launched Project Crypto to study on-chain market infrastructure.

The SEC announces the launch of "Project Crypto"

- SEC Chair Paul Atkins announced the agency is exploring regulatory adjustments to support tokenization, while Commissioner Hester Peirce reiterated that tokenized securities remain under traditional laws.

SEC's Pierce on Tokenization, Bitcoin in 401(k) Accounts

Interpretation: the policy direction points toward integrating tokenized instruments into existing securities frameworks rather than creating a parallel regime.

United Kingdom

- The UK continued advancing its Digital Securities Sandbox (DSS), a joint initiative by the Bank of England and FCA that allows firms to pilot tokenized securities activities under a regulated framework.

Asia-Pacific

Across Singapore, Hong Kong, Australia, and Japan, regulators progressed in defining legal frameworks for tokenized finance.

- Singapore and the UK deepened Project Guardian collaboration around open, interoperable networks.

- Hong Kong is considering Basel III flexibility to allow banks to hold stablecoins and use public blockchains.

- Hong Kong also launched a new RWA platform under its Web3 Standardization Association.

- Also in Hong Kong, the HKMA announced that the first stablecoin licenses could arrive in early 2026.

- Project Acacia (a joint initiative between the Reserve Bank of Australia and the Digital Finance Cooperative Research Centre) announced selected industry participants to experiment 24 innovative use cases focused on RWA tokenization.

- Japan’s FSA is set to approve the first yen-backed stablecoin (JPYC), pegged 1:1 to JPY and backed by liquid assets such as bank deposits and Japanese government bonds.

- Japan’s FSA also plans to introduce a crypto bill by 2026.

Interpretation: APAC continues to prioritize supervised experimentation, with settlement assets and identity frameworks as near-term focus areas.

Middle East and Oceania

- Dubai’s DFSA approved the region’s first tokenized money market fund, issued by QNB and DMZ Finance.

- New Zealand launched a public consultation on how tokenized financial products should be regulated.

2. Tokenized Stocks and ETFs Gain Momentum

The tokenization of stocks and ETFs continued evolving this quarter, following a wave of developments by Robinhood, Kraken, Gemini, Coinbase, and Bybit in Q2. Proposals from incumbent venues indicate growing willingness to test multiple tokenization approaches.

- eToro added 245 new tokenized instruments, including stocks and futures, reinforcing the shift toward 24/7 asset access.

- Coinbase plans to offer tokenized U.S. stocks and prediction markets, pending regulatory approval.

- Ondo Global Markets, an affiliate of Ondo Finance launched over 100 tokenized US stocks and ETFs on-chain, available to non-U.S. investors.

- 21Shares filed for the first-ever U.S. ETF tracking an RWA-focused token (ONDO).

- BlackRock is evaluating how to tokenize ETFs, signaling further institutional movement toward digital fund structures.

- The Vietnam-focused asset manager Dragon Capital ($5.5 billion AUM) announced a proposal for the pilot project that tokenizes exchange-traded funds (ETFs)

- Also in the U.S., Nasdaq formally submitted a proposal to the SEC to list tokenized versions of stocks on its markets. If approved, it would enable dual-format trading: the current digital system and a blockchain-based tokenized alternative, under the same order book, execution priority, and shareholder rights.

Back at STO Summit Korea, InvestaX CEO Julian Kwan broke down how tokenized shares reshape who can access and issue public equities. Watch the interview below.

InvestaX CEO Julian Kwan on tokenized stocks

From a regulatory lens, the SEC’s Hester Peirce stated that the agency remains open to "multiple models of securities tokenization", allowing the market to experiment under existing securities law frameworks. [Watch the interview]

3. Money Market Funds and Institutional Use Cases Expand

MMFs are moving from passive holdings to active collateral in credit workflows. The practical benefit is intraday mobility and cleaner audit trails, not headline “speed” alone.

- Goldman Sachs and BNY Mellon teamed up to issue tokens representing shares in major institutional MMFs, joined by firms like BlackRock and Fidelity.

- DBS Bank announced plans to allow institutional clients to use Franklin Templeton’s tokenized MMF as loan collateral, a major step in fund utility expansion.

- Binance now supports tokenized RWAs - USYC and cUSDO - as off-exchange, yield-bearing collateral.

- Kaio tokenized $3B in funds on Hedera, reinforcing the shift from pilot projects to production-grade RWA platforms.

4. New Players and Asset Classes Signal Wider Use Cases

Beyond fixed income, sectors with complex cash-flow rights and audit needs are testing tokenization for better data integrity and lifecycle management.

- In China, AntChain tokenized $8.4B in carbon-neutral energy assets, showcasing tokenization’s role in industrial ESG strategies.

- In Japan, Mitsubishi UFJ Trust and Banking, the trust division of MUFG plans to tokenize real estate and sell tokenized real estate to both retail and institutional investors.

- In Singapore, OCBC became the first bank to offer tokenized bonds to corporate accredited investors. Minimum investment thresholds were lowered from the usual S$250,000 to S$1,000.

- IVD Medical and Transcenta launched a pilot to tokenize pharma R&D assets and drug cash flows, marking one of the first attempts to apply tokenization in life sciences.

- Asset manager GuoFu Quantum has launched a tokenized investment fund under Hong Kong’s regulatory framework.

- Singapore-based MetaComp and Hong Kong’s OSL partnered to build a cross-border tokenized finance stack across Singapore and Hong Kong.

5. Infrastructure Investment and Settlement Networks Evolve

- Boerse Stuttgart Group launched Seturion, a pan-European settlement platform for tokenized assets, aiming to solve Europe’s fragmented infrastructure.

- Wall Street firms executed the first 24/7 tokenized Treasury financing pilot via Canton Network, signaling how institutional finance is adopting tokenized rails.

- Circle and Stripe announced plans to build native blockchain networks to better support stablecoins and tokenized payments.

- USDC stablecoin went live on the XDC Network, expanding enterprise-grade payment and tokenization use cases.

Settlement assets and connectivity layers are becoming the strategic battleground. The institutions building rails for tokenized MMFs and Treasuries often shape what scales next.

Stablecoin: Driving a Financial Services Revolution

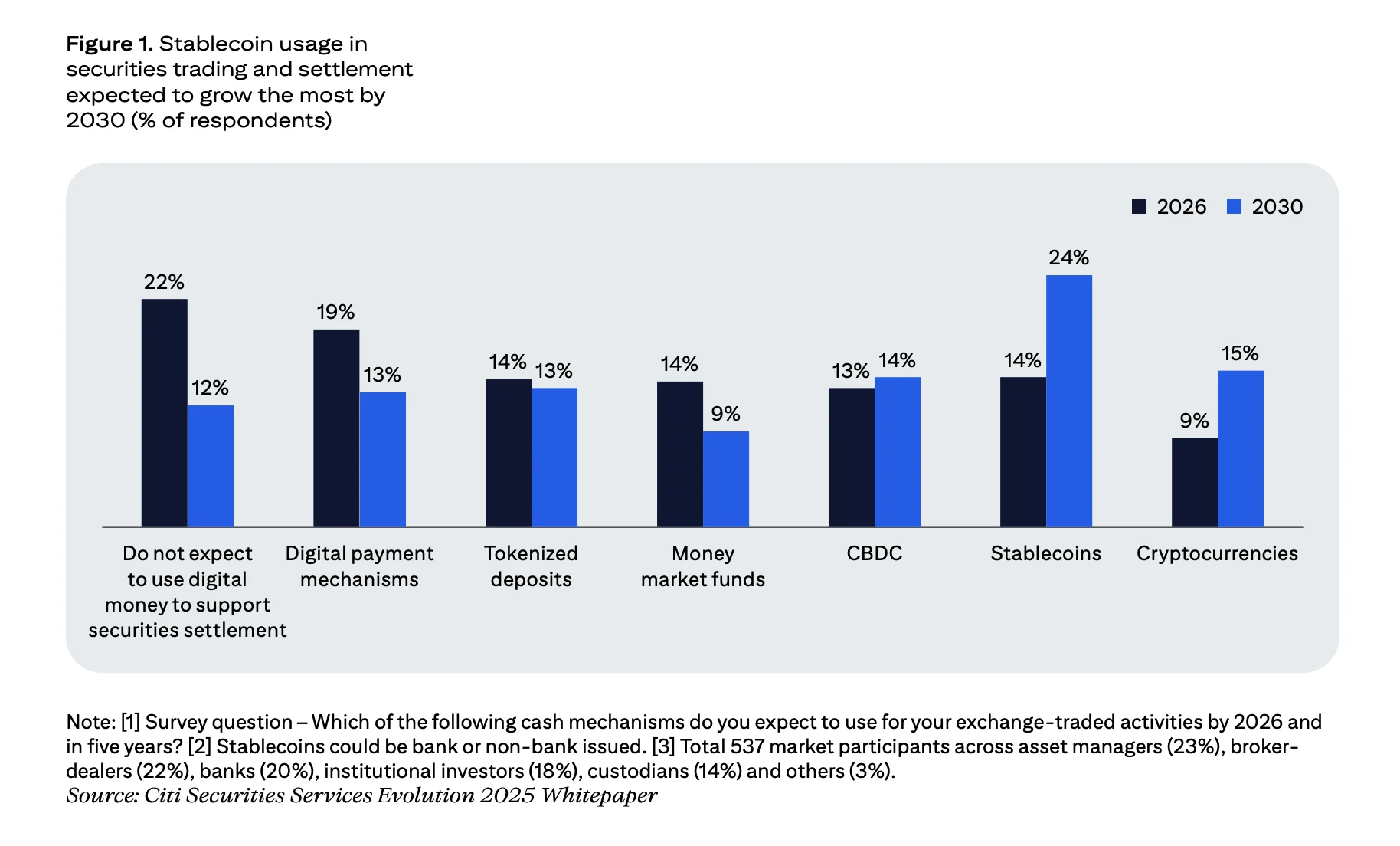

Stablecoins continued to establish themselves this quarter as core components of financial infrastructure. Their role is expanding from simple payment rails to settlement layers and, increasingly, as entry points into tokenized assets.

According to McKinsey’s The Stable Door Opens report, stablecoins are well-positioned for institutional-grade use cases across treasury, payments, and post-trade settlement. Citi’s Future of Post-Trade (Sept 2025) similarly found that stablecoins are expected to grow faster than any other digital money format in securities trading and settlement by 2030. Both studies reinforce what was visible on-chain this quarter, where tokenized MMFs and Treasuries were actively paired with stablecoins in collateral and repo flows.

Stablecoins were among major topics in live stage conversations this quarter. InvestaX COO Alice Chen joined industry panels hosted by SwissCham Singapore and Gibson Dunn to assess stablecoin standards, ecosystem risks, and interoperability needs. The participation underscores how regulators and institutions are treating stablecoins not as fringe instruments, but as part of the market architecture supporting tokenization.

Jurisdictions are also taking steps to formalize frameworks regulating stablecoins.

- In the U.S., the GENIUS Act advanced to regulate reserve-backed stablecoins.

- Japan is preparing to approve JPYC, its first yen-backed stablecoin.

- Hong Kong is designing a licensing regime and Basel III flexibility for banks to hold stablecoins.

- South Korea is drafting a law on issuance, collateral, and controls.

Together these moves show regulators aligning stablecoin design with existing prudential standards, creating a stronger foundation for their use in tokenized markets.

Stablecoins and RWA Tokenization: A Structural Link

For tokenization, the implications are emerging:

- Collateral: Stablecoins act as cash equivalents for borrowing against tokenized assets.

- Settlement: Instant settlement between stablecoins and RWAs increases efficiency across platforms.

- Programmability: Stablecoins allow for automation of fund flows in tokenized credit, lending, and structured products.

As regulatory frameworks tighten and adoption expands, stablecoins are likely to remain one of the most active categories within tokenized finance, both as a cash layer and a compliance-aligned bridge to real-world asset markets.

Recent RWA Reports for Further Context

This quarter, several major institutions released research that frames tokenization as a near-term evolution in capital markets, payments, and post-trade infrastructure. These 2025 RWA tokenization reports offer useful reference points for those building or investing in digital asset infrastructure.

1. World Economic Forum - Asset Tokenization in Financial Markets 2025

The WEF outlines how tokenization is already scaling across fixed income, real estate, and funds. The report emphasizes how tokenized assets are becoming integrated into regulated financial systems.

Read report

2. Citi - The Future of Post-Trade

Over 80% of market participants surveyed believe digital assets and distributed ledger technology (DLT) will reshape market structure. Tokenized money, like stablecoins, MMFs, and tokenized deposits, is seen as essential for real-time settlement. As markets shift to T+1 (and beyond), tokenization may offer faster settlement, collateral mobility, and lower costs.

Read report

3. McKinsey - The Stable Door Opens: How Tokenized Cash Enables Next-Gen Payments

Stablecoins and tokenized deposits are being embedded into next-generation payment rails. This report explains how tokenized cash unlocks programmability and interoperability, and why regulated use cases are quickly becoming the focus.

Read report

4. GFMA - Joint Industry Call for Recalibration of Crypto Prudential Rules

Global trade bodies argue for a more nuanced approach to crypto prudential standards. The paper notes that DLT can support safer, more efficient markets, and that tokenization has the potential to reduce settlement times, improve liquidity, and strengthen operational resilience.

Read statement

What’s Next?

Q3 showed a market that is consolidating where it already fits institutional needs: short-duration credit, Treasuries, and MMFs. The next phase will likely depend on how well settlement, custody, and regulatory frameworks align to support scaled secondary markets.

Settlement assets

As stablecoin and tokenized cash frameworks mature, we expect larger bilateral and tri-party flows to move on-chain, particularly in repo and collateral upgrades. This does not require wholesale replacement of existing systems. It requires reliable convertibility between rails, clearer finality, and standardized controls.

Custody and controls

Institutions new to on-chain finance continue to ask about key risk and operational continuity. The practical answer is qualified custody, policy-based wallet management, and asset-level controls. Where regulated custodians and licensed platforms coordinate, we see faster institutional onboarding and clearer audit rights.

Secondary market design

Liquidity remains a work-in-progress. For many strategies, tokenization is delivering value through servicing and compliance automation first. As product terms, market-making models, and investor access improve, secondary activity should follow. The likely path is product-by-product, starting with standardized instruments and clear redemption mechanics.

Tokenization today is not about inventing new assets but about upgrading issuance, servicing, and distribution. Institutions should work with a licensed asset tokenization platform that embeds compliance and governance aligned with existing frameworks.

What is the RWA tokenization market size?

The real-world asset (RWA) tokenization market is valued at ~$35.78 billion as of November 2025, according to RWA.xyz. This metric showcases significant expansion, increasing approximately 10x since the total market value was $2.9 billion in 2022.

What is the tokenized U.S. treasuries market size?

As of October 31 2025, the tokenized U.S. Treasury market has expanded to $8.8 billion. BlackRock USD Institutional Digital Liquidity Fund is currently the largest tokenized U.S. treasuries project by total asset value, with ~$2,8 billion, followed by Circle USYC with $990 million and Franklin OnChain U.S. Government Money Fund with $850 million.

Which tokenized asset classes are growing the fastest?

According to RWA.xyz data, tokenized U.S. Treasuries are currently the fastest-growing asset class, as of October 31, 2025. The value of tokenized Treasuries reached $8.7 billion, up from $2.48 billion a year earlier, representing a 251% year-on-year increase.

Private credit remains the largest category, growing from $13.67 billion to $18.7 billion over the same period - a ~37% increase. Commodities also showed solid momentum, doubling from $1.1 billion to $2.9 billion, a 164% increase.

Which public blockchains are most commonly used for tokenized RWAs today?

Provenance and Ethereum are currently the two leading public blockchains for tokenized RWAs. Provenance hosts over $12 billion in tokenized assets, while Ethereum supports major issuers like BlackRock, Franklin Templeton, Ondo, and Backed, with more than $9.5 billion in tokenized asset value.